⏩ stepit 'naive': Starting execution of `strom.modelling.assess_model()` 2026-04-12 13:37:03 ⏩ stepit 'get_single_split_metrics': Starting execution of `strom.modelling.get_single_split_metrics()` 2026-04-12 13:37:04 ✅ stepit 'get_single_split_metrics': Successfully completed and cached [exec time 0.0 seconds, cache time 0.0 seconds, size 1.0 KB] `strom.modelling.get_single_split_metrics()` 2026-04-12 13:37:04 ⏩ stepit 'cross_validate_pipe': Starting execution of `strom.modelling.cross_validate_pipe()` 2026-04-12 13:37:04 [Parallel(n_jobs=-1)]: Using backend LokyBackend with 4 concurrent workers. [Parallel(n_jobs=-1)]: Done 5 out of 5 | elapsed: 2.1s finished ✅ stepit 'cross_validate_pipe': Successfully completed and cached [exec time 2.1 seconds, cache time 0.0 seconds, size 2.2 KB] `strom.modelling.cross_validate_pipe()` 2026-04-12 13:37:06 ✅ stepit 'naive': Successfully completed and cached [exec time 2.2 seconds, cache time 0.0 seconds, size 15.7 KB] `strom.modelling.assess_model()` 2026-04-12 13:37:06

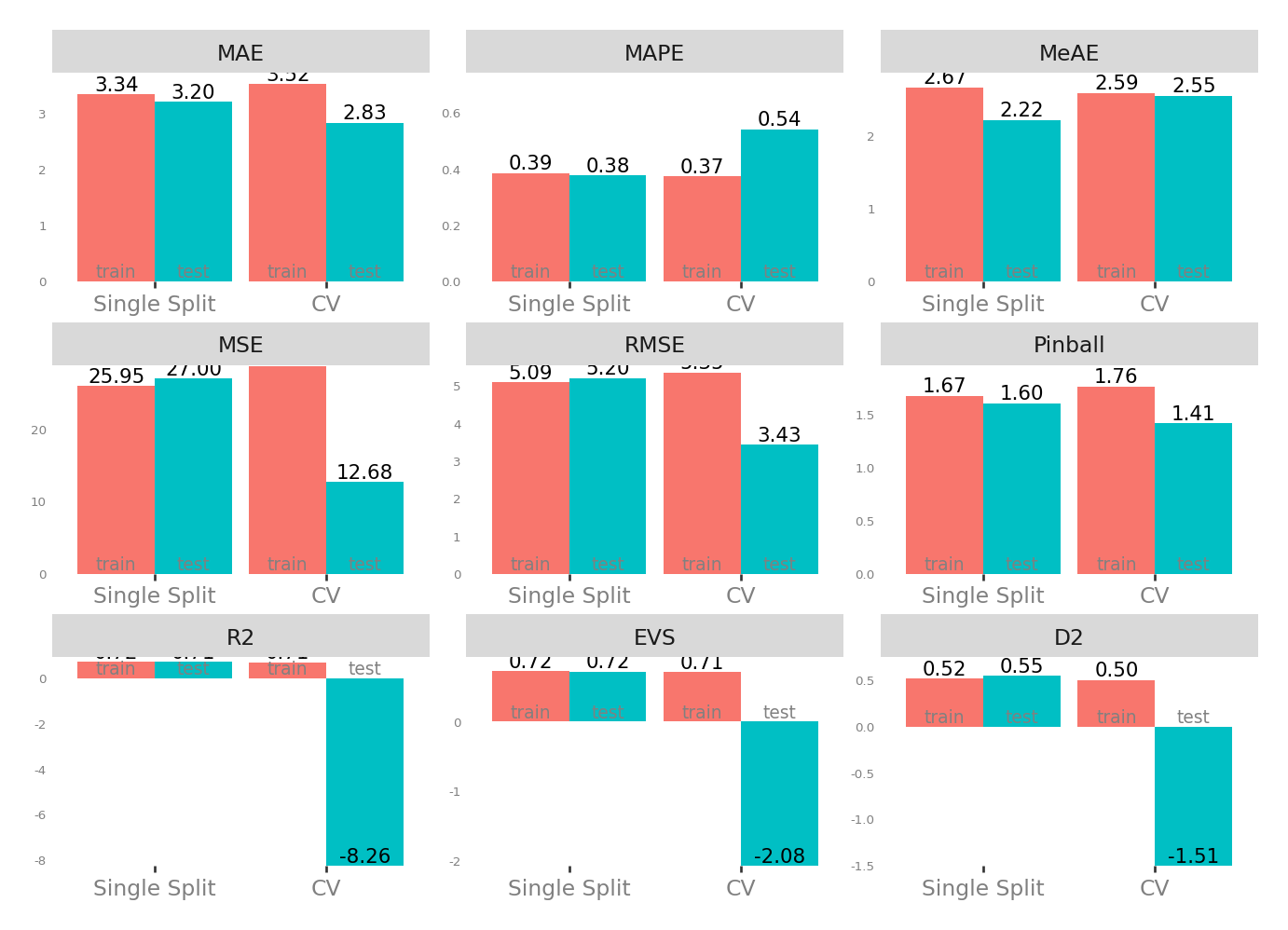

Naive Model

Naive model

A simple OLS model with temperature and air humidity, without any transformation or feature engineering -no thinking at all-.

Metrics

| Single Split | CV | |||

|---|---|---|---|---|

| train | test | test | train | |

| MAE - Mean Absolute Error | 3.340488 | 3.162185 | 2.826249 | 3.521145 |

| MSE - Mean Squared Error | 25.947551 | 24.493693 | 12.676356 | 28.646140 |

| RMSE - Root Mean Squared Error | 5.093874 | 4.949110 | 3.426344 | 5.349381 |

| R2 - Coefficient of Determination | 0.721589 | 0.749748 | -8.271677 | 0.710541 |

| MAPE - Mean Absolute Percentage Error | 0.385556 | 0.325290 | 0.541985 | 0.374222 |

| EVS - Explained Variance Score | 0.721589 | 0.749876 | -2.079990 | 0.710541 |

| MeAE - Median Absolute Error | 2.667506 | 2.272731 | 2.553267 | 2.588375 |

| D2 - D2 Absolute Error Score | 0.517747 | 0.587819 | -1.510111 | 0.504172 |

| Pinball - Mean Pinball Loss | 1.670244 | 1.581092 | 1.413125 | 1.760573 |

Scatter plot matrix

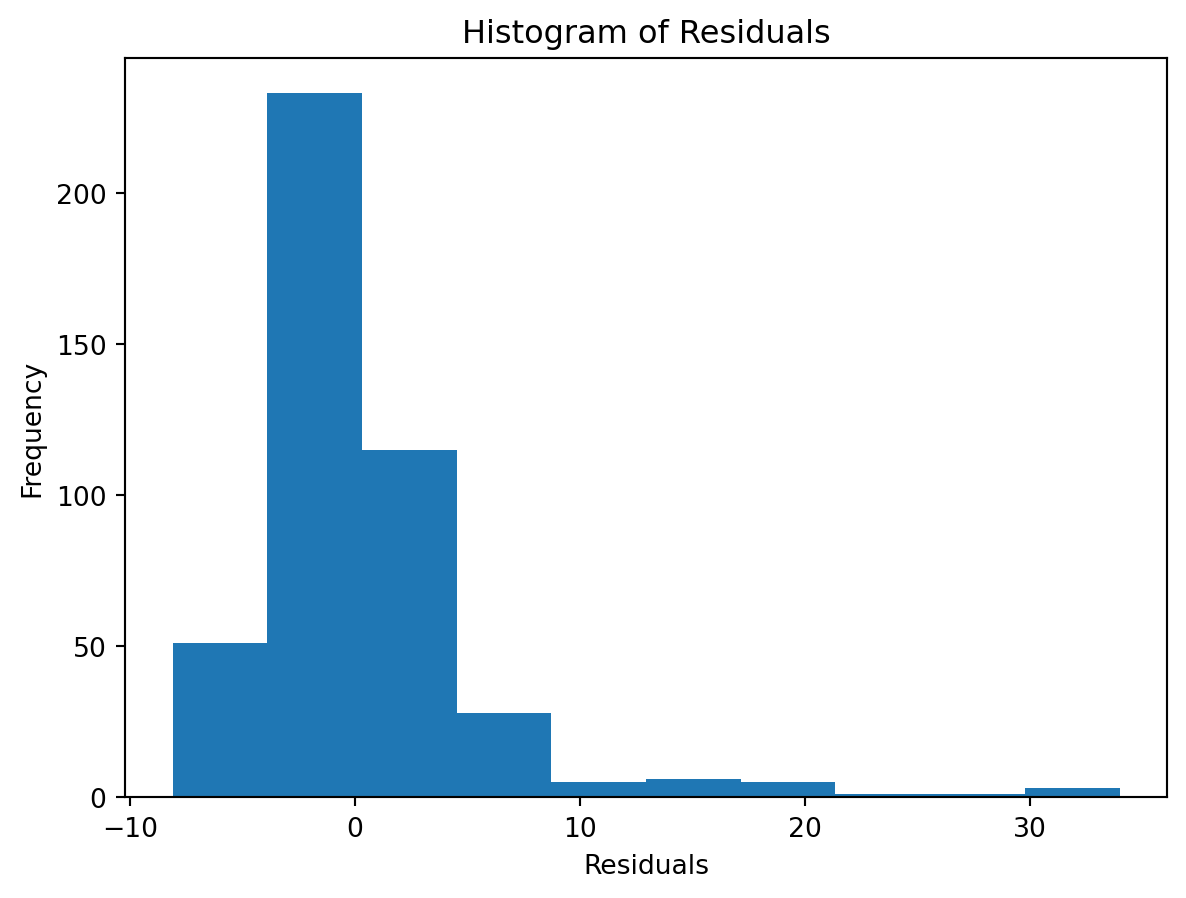

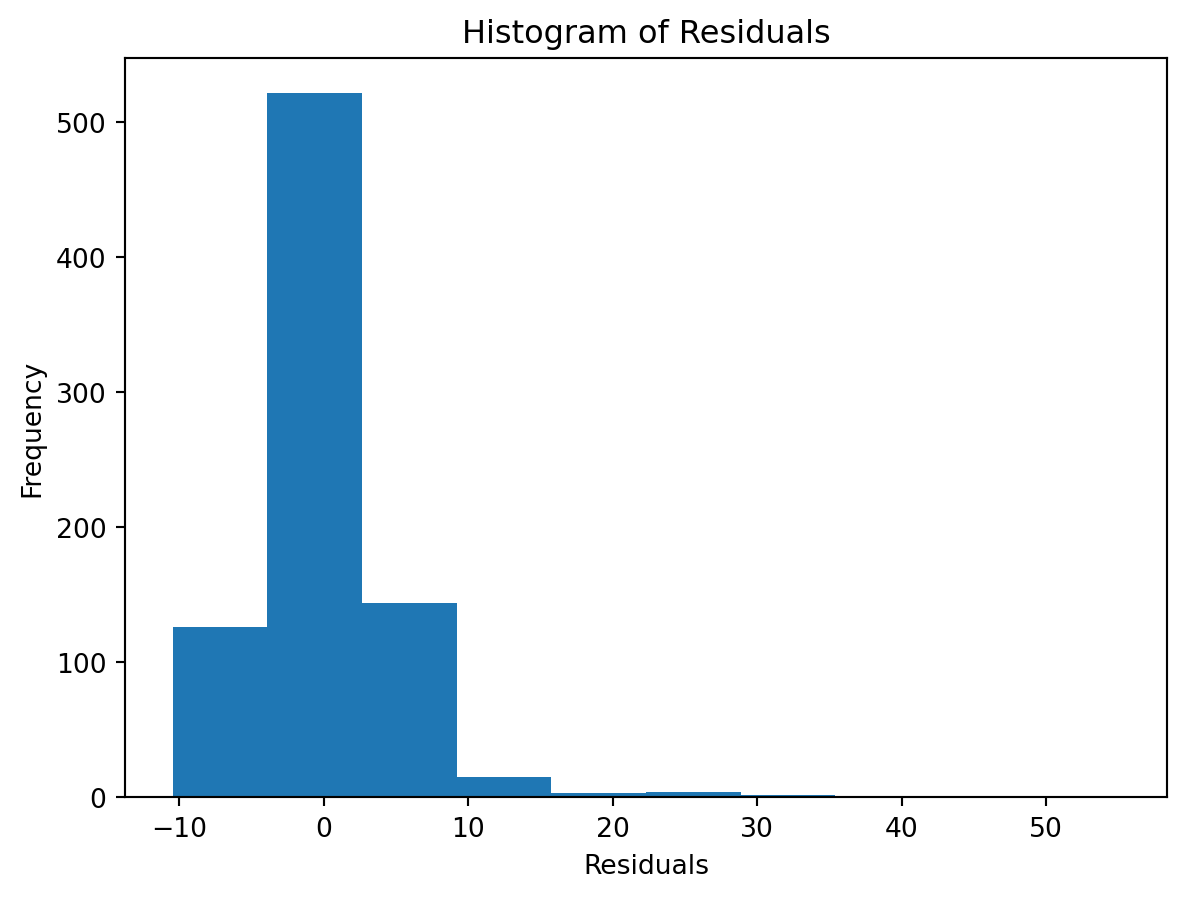

Observed vs. Predicted and Residuals vs. Predicted

Check for …

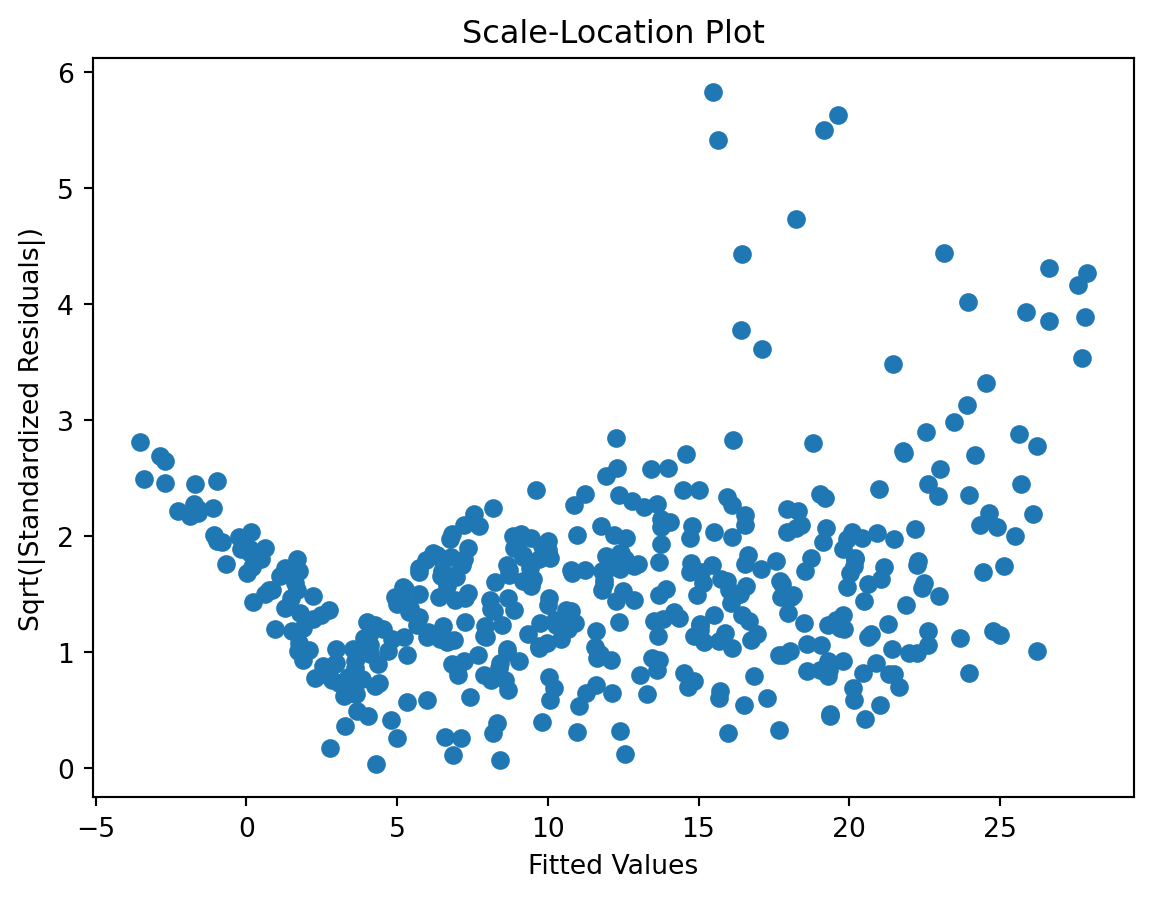

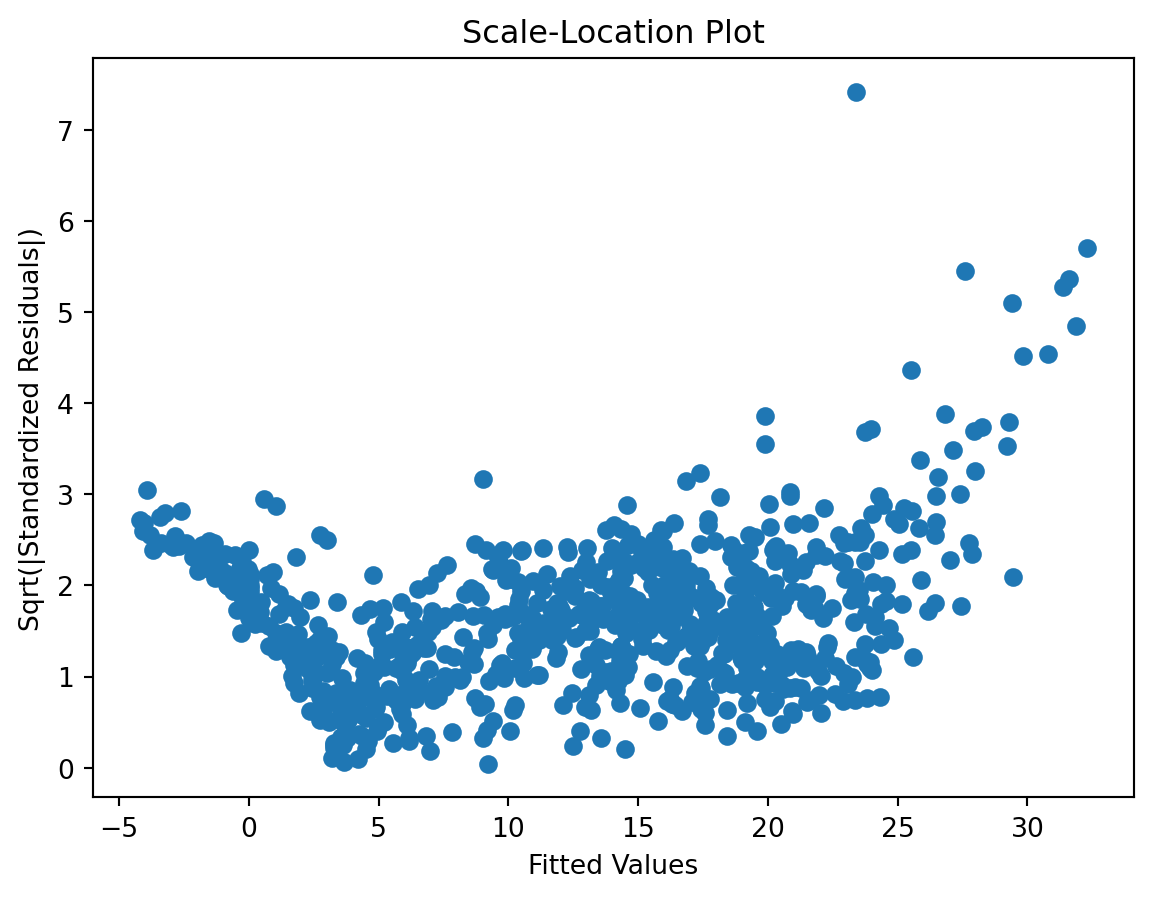

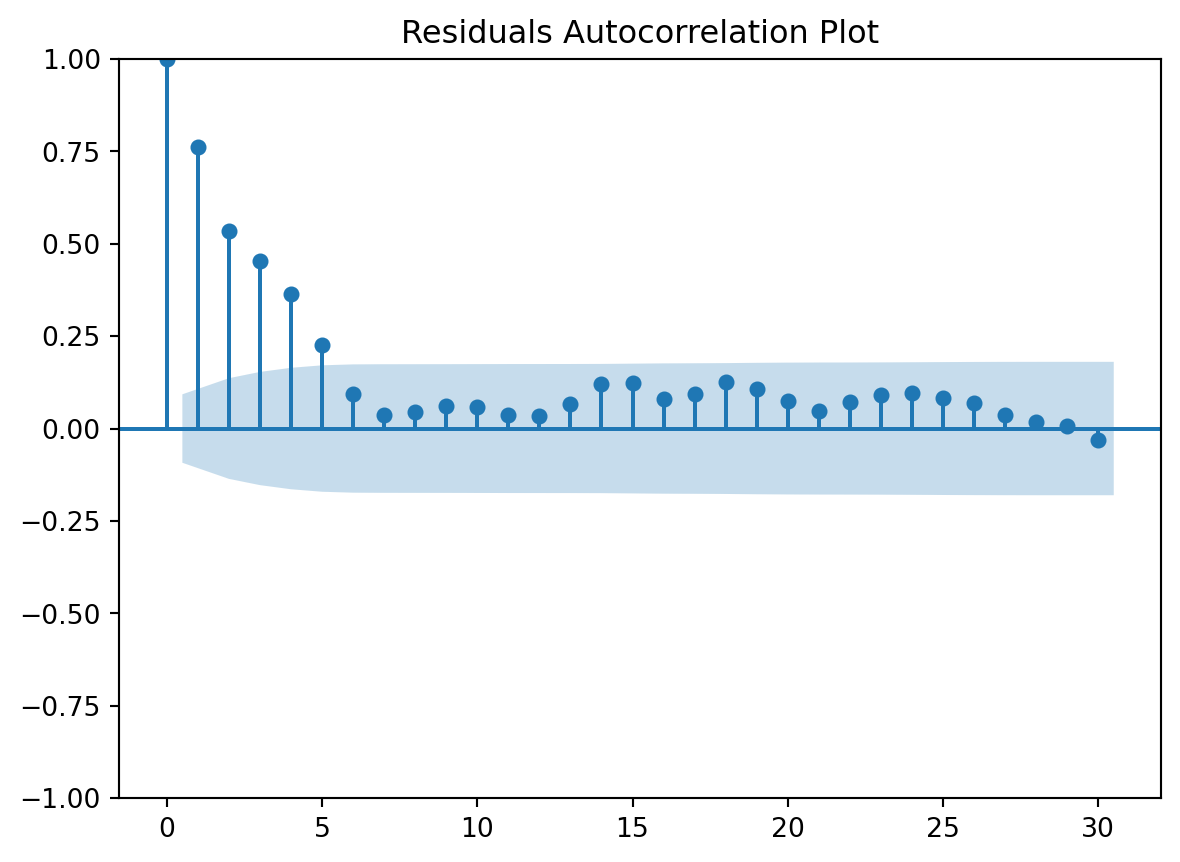

check the residuals to assess the goodness of fit.

- white noise or is there a pattern?

- heteroscedasticity?

- non-linearity?

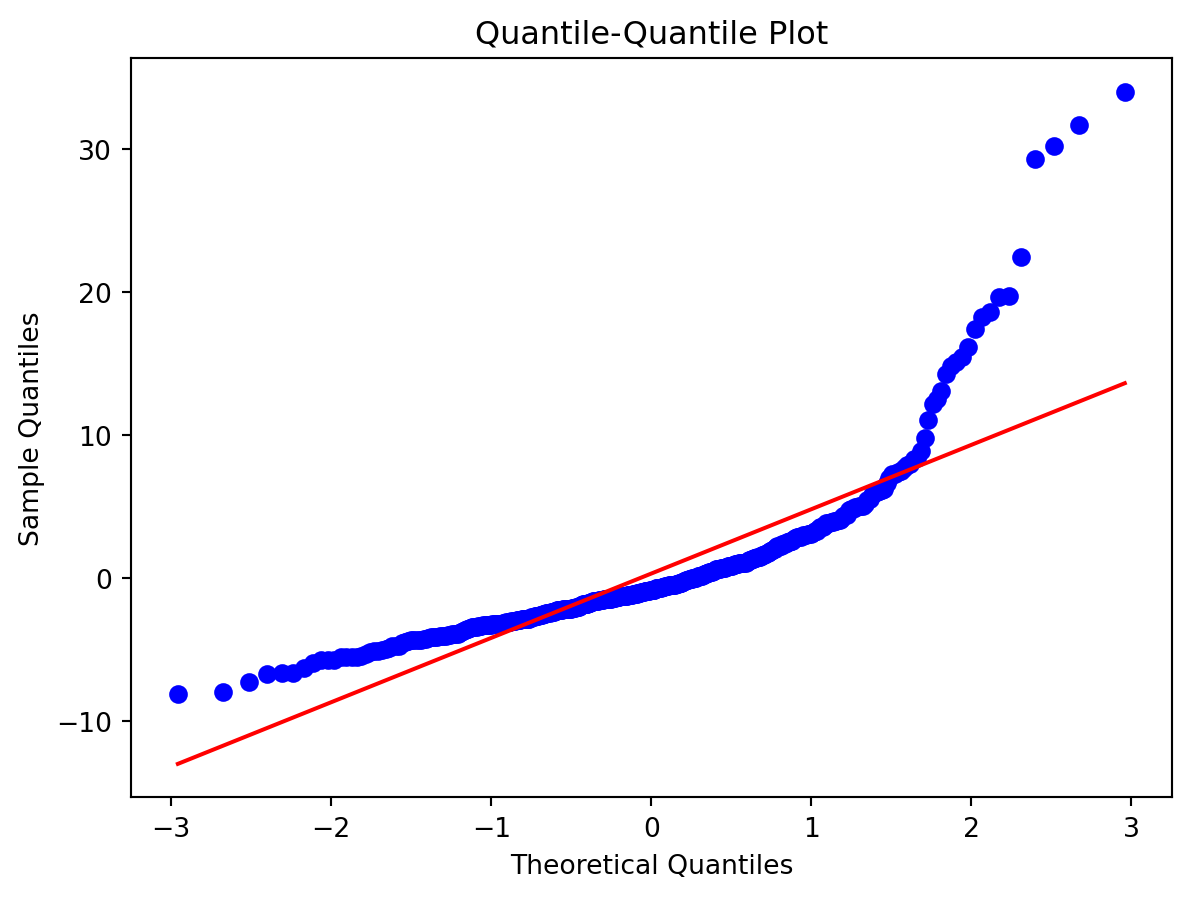

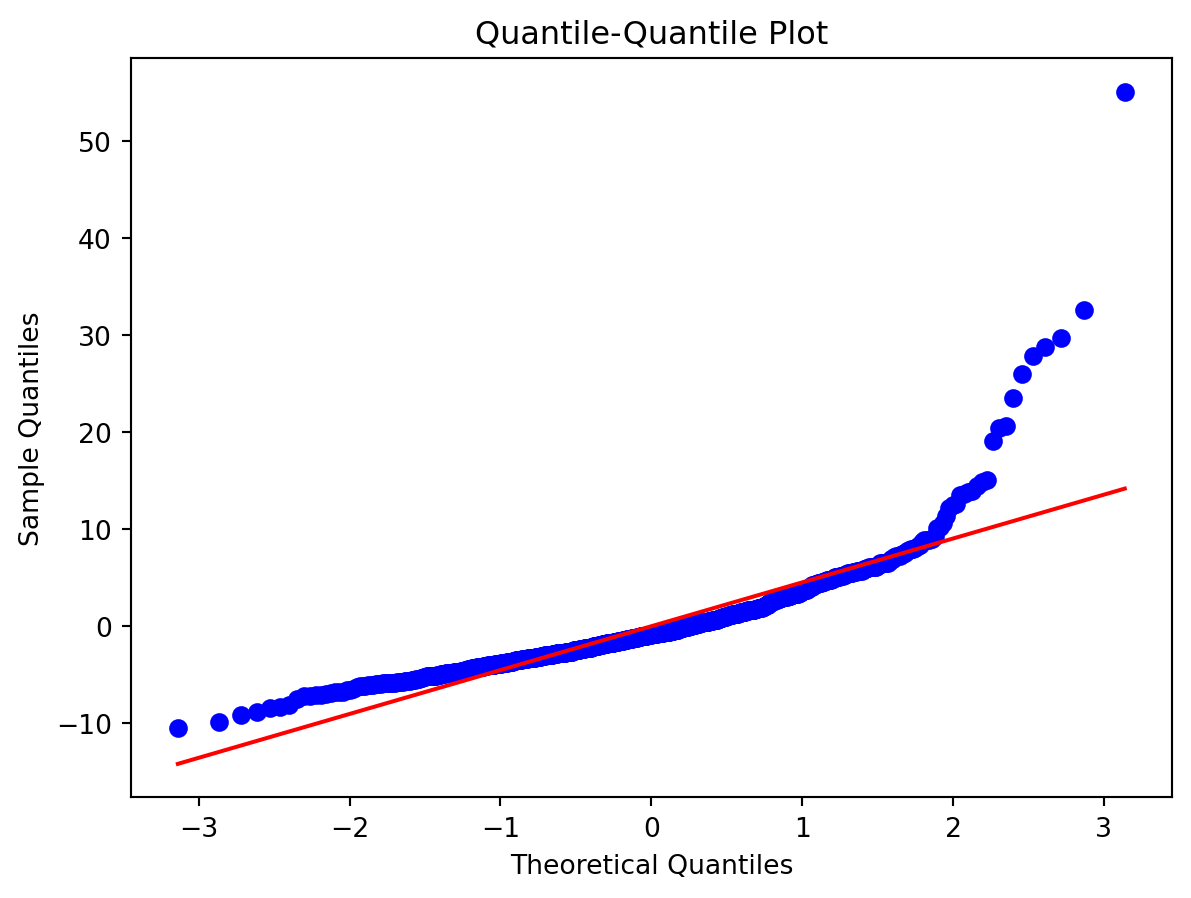

Normality of Residuals:

Check for …

- Are residuals normally distributed?

Leverage

Scale-Location plot

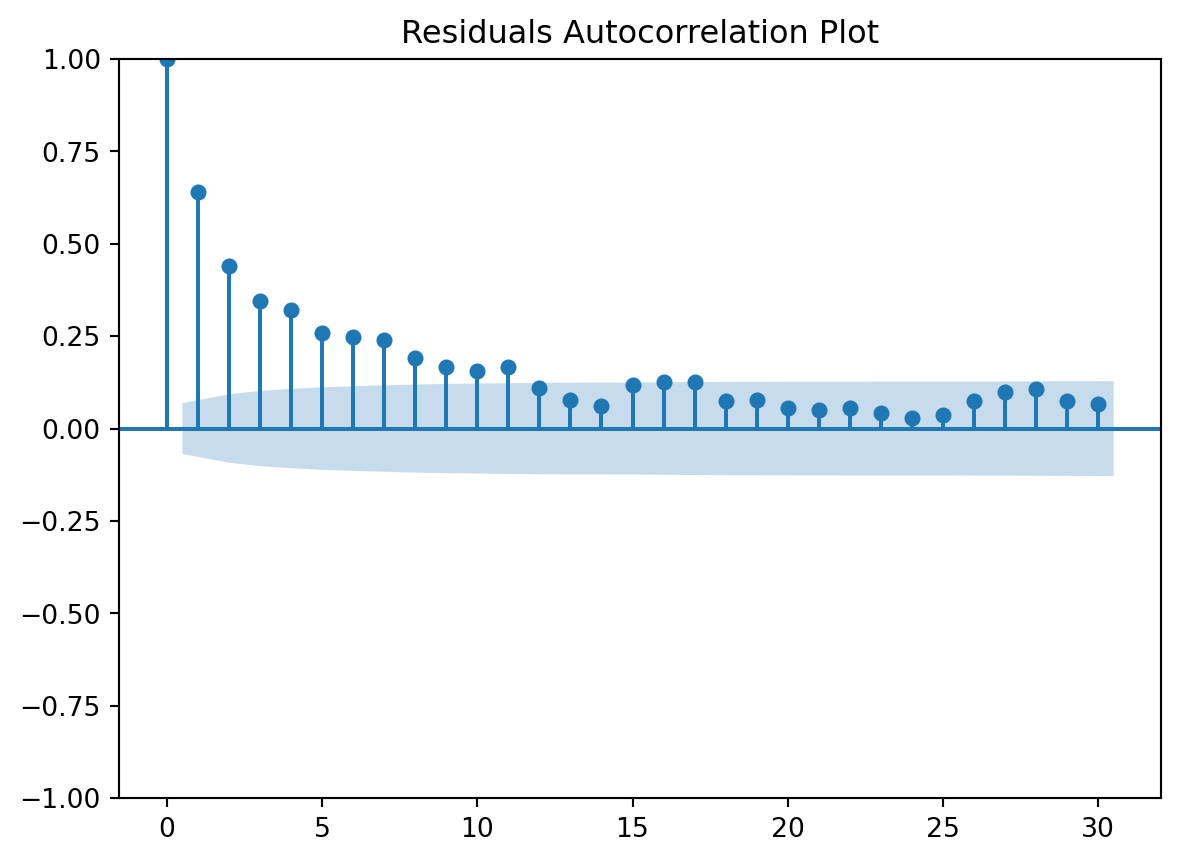

Residuals Autocorrelation Plot

Residuals vs Time

TODOs

Clearly the naive model is not a good fit (as expected).

Naive Model, but using statsmodels …

OLS Regression Results

==============================================================================

Dep. Variable: wd R-squared: 0.737

Model: OLS Adj. R-squared: 0.737

Method: Least Squares F-statistic: 1963.

Date: Sun, 12 Apr 2026 Prob (F-statistic): 0.00

Time: 13:37:10 Log-Likelihood: -4259.4

No. Observations: 1405 AIC: 8525.

Df Residuals: 1402 BIC: 8541.

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 27.9188 1.219 22.899 0.000 25.527 30.310

tt_tu_mean -1.1363 0.019 -59.272 0.000 -1.174 -1.099

rf_tu_mean -0.0612 0.014 -4.300 0.000 -0.089 -0.033

==============================================================================

Omnibus: 979.383 Durbin-Watson: 0.631

Prob(Omnibus): 0.000 Jarque-Bera (JB): 21072.270

Skew: 2.959 Prob(JB): 0.00

Kurtosis: 21.026 Cond. No. 737.

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

R-squared: 0.7368832968577501Naive model, but using scikit-learn without pipeline …